IC-DISC Explained – 2026 Guide to Export Tax Savings & IRS Rules

For U.S. exporters, the Interest Charge Domestic International Sales Corporation (IC-DISC) remains a powerful but often underutilized tax savings tool. Originally enacted by Congress in 1971, it stands as the last significant federal incentive designed specifically to bolster businesses selling goods or services globally.

This 2026 practical guide is designed to help you navigate the current IRS filing cycle and commission reporting requirements, ensuring your business stays ahead of the latest exporter planning concerns. Whether you are looking to optimize your IC-DISC tax strategy or need immediate planning assistance via video conference, securing your export benefits starts with proactive implementation.

Why IC-DISC Matters Now? By leveraging an IC-DISC, eligible companies can significantly reduce tax liabilities, improving cash flow and overall profitability. This 2026 guide reflects the current IRS filing and reporting framework, including the latest Form 1120-IC-DISC and Schedule P commission reporting requirements released in January 2026. Whether you own a manufacturing company, an engineering firm, or a business that exports U.S.-made products, understanding how IC-DISC is explained in the context of modern regulations can unlock substantial financial benefits.

Below, we provide a comprehensive breakdown of how the mechanism works, who qualifies under today’s standards, and how to maximize your savings for the current fiscal year.

Understanding IC-DISC: A Step-by-Step Guide:

- What Is an IC-DISC?

- How the IC-DISC Works

- Visual Guide

- Why IC-DISC Results in Significant Export Tax Savings

- Who Qualifies for IC-DISC?

- Which Products and Services Qualify for IC-DISC?

- How to Determine If Your Business Qualifies

- How to Set Up an IC-DISC (and Stay Compliant)

- Why Work with a Specialist?

- How IC-DISC Commissions Are Calculated

- Compliance and Reporting Requirements

- Potential Risks & Challenges of IC-DISC

- State Tax Implications of IC-DISC

- IC-DISC vs. Other Export Tax Incentives

- How to Maximize IC-DISC Benefits

- Quick Answers to Common IC-DISC Questions

- Conclusion & Next Steps

What Is an IC-DISC?

An IC-DISC, or Interest Charge Domestic International Sales Corporation, is a tax-exempt corporate structure authorized by Section 992 of the U.S. Internal Revenue Code to promote domestic exports. It remains the core statutory incentive still available to U.S. exporters, enabling qualifying companies to reduce their federal income tax liability by reclassifying a portion of export profits. Under this framework, these profits are distributed as qualified dividends, which are generally taxed at significantly lower rates than ordinary income.

While the IC-DISC doesn’t operate like a traditional business with employees or office space, it is a vital component of a modern tax strategy. In the current 2026 filing and reporting environment, the process remains highly effective:

- The Setup: A U.S. exporter establishes a separate IC-DISC entity.

- The Commission: The exporter pays a commission to the IC-DISC based on qualifying export sales and deducts that commission from its taxable income.

- The Distribution: The IC-DISC, which pays no federal income tax, passes these earnings to its shareholders.

This mechanism yields substantial export tax savings without requiring any changes to your underlying business operations.

Since 1971, the IC-DISC has stood as the only permanent federal tax incentive specifically for exporters. Despite being underutilized, it offers a major competitive advantage to eligible companies in manufacturing, distribution, and architectural or engineering services. As we look toward the future of IC-DISC, it continues to be an essential tool for domestic firms competing globally.

Deep Dive: For a more technical breakdown of how to maintain compliance, see our comprehensive IC-DISC rules and requirements. You can also review the IRS overview for Form 1120-IC-DISCto see the latest 2026 reporting updates.

Watch our video to learn more about the benefits of IC-DISC explained:

How the IC-DISC Works: A 2026 Step-by-Step Breakdown

At its core, the IC-DISC structure allows exporters to legally shift taxable export income into a lower tax bracket by utilizing a separate, tax-exempt corporate entity. In the 2026 tax landscape, maintaining rigorous documentation for each step is essential for compliance and maximizing your return.

Step 1: Confirm Qualified Export Sales

Your business sells goods or services for use outside of the United States. These can be direct sales to foreign customers or indirect sales to domestic customers who then export the product. To qualify, you must verify qualified export receipts and ensure the goods meet export property regulations, including the requirement that at least 50% of the value is U.S.-sourced.

- 2026 Update: Ensure you have contemporaneous “foreign use” certificates or shipping documentation to support these receipts during the current filing cycle.

Step 2: Calculate and Document the Commission

The operating company pays a commission to its IC-DISC based on qualified export sales. This amount is determined using IRS-approved commission calculation methods, such as the 4% of gross receipts or 50% of export income method.

- Compliance Note: Under IC-DISC commission payment rules, the method used must be documented and supportable to justify the deductible business expense that lowers your operating company’s taxable income.

Step 3: The IC-DISC Receives Tax-Exempt Income

The IC-DISC itself pays no federal income tax on the commission it receives. To maintain this status, the entity must strictly satisfy the DISC requirements under Section 992. While the entity is a C Corporation, it does not require employees, office space, or inventory to function as a valid tax-planning vehicle.

Step 4: Strategize Distributions to Shareholders

The IC-DISC then distributes its income to its shareholders, typically the same owners as the operating company, as qualified dividends.

- Planning Insight: In 2026, IC-DISC distributions and retained earnings carry different planning consequences. While distributions trigger the dividend tax rate, retaining earnings may trigger an IC-DISC interest charge, which is often a strategic choice for deferring larger tax liabilities.

Step 5: Realize the Tax Arbitrage

The final result is a significant reduction in federal taxes. Qualified dividends are generally taxed at lower rates (often 20%) compared to ordinary income rates (up to 37%), creating an effective savings of 10% to 17% or more.

- Individual Impact: The exact lower-rate treatment depends on specific shareholder-level tax facts and total taxable income for the 2026 tax year.

See it in action: Review a real-world IC-DISC example to see how these steps translate into actual bottom-line savings for a mid-sized exporter.

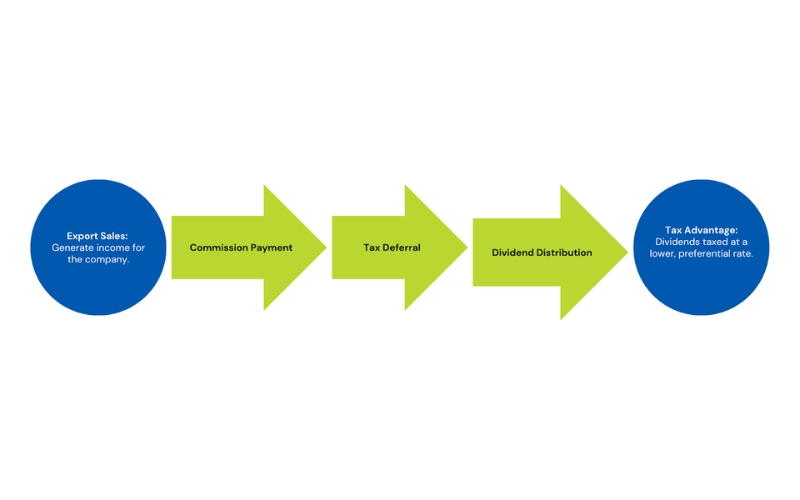

Visual Guide: Understanding the Tax Flow and Commission Structure

To simplify the process, we have provided a high-level educational map that illustrates the tax flow and commission structure step-by-step.

Important 2026 Compliance Note: This visual is designed for conceptual understanding and is not a substitute for the rigorous annual commission calculation and reporting workpapers required by the IRS. Under current 2026 regulations, taxpayers must still file detailed annual returns via Form 1120-IC-DISC and maintain supporting schedules for all transactions.

The Transactional Path:

- Start: Export sales generate income for the operating company.

- Commission Payment: The exporting company pays a deductible commission to the IC-DISC for facilitating export transactions.

- Tax Deferral: The IC-DISC’s income is tax-exempt at the federal level. It remains untaxed until distributed as dividends (or subject to the annual interest charge if earnings are retained).

- Dividend Distribution: When the IC-DISC distributes earnings to the shareholders, those distributions are categorized as qualified dividends.

- Tax Advantage: Because these dividends are taxed at preferential rates, often significantly lower than standard ordinary income or corporate tax rates, the structure provides substantial, permanent tax savings.

This structure remains a game-changer for exporters and professionals who fully master its intricacies. For exporters, it is a primary lever to maximize cash flow. For accountants, understanding how IC-DISC is explained in today’s regulatory environment allows for the delivery of unparalleled value to clients through sophisticated tax accounting.

Why IC-DISC Results in Significant Export Tax Savings

The effectiveness of an IC-DISC lies in a simple but powerful mechanism: it allows U.S. exporters to recharacterize a portion of their export profits as qualified dividends. In the 2026 tax landscape, these dividends continue to be taxed at preferential rates compared to ordinary business income.

While individual results vary based on your specific taxpayer structure and Net Investment Income Tax (NIIT) exposure, this rate differential often leads to substantial federal income tax savings for eligible export income.

Ordinary Income vs. Qualified Dividend Rates

The following table illustrates the potential arbitrage between income types for the 2026 filing year:

| Income Type | Maximum Federal Tax Rate |

| Ordinary Business Income | Up to 37% |

| Qualified Dividends | Up to 20% (plus 3.8% NIIT) |

Instead of being taxed at the higher ordinary income rate, export profits routed through an IC-DISC are distributed to shareholders. As noted in IRS Topic 404, these distributions are generally treated as qualified dividends, significantly lowering the effective tax burden for many owners. For S Corporation or pass-through entity owners, this income flows directly to individual returns while retaining its lower-rate status.

Key Financial Drivers of the IC-DISC

- Tax-Exempt Status at the Entity Level: The IC-DISC is a federally tax-exempt corporation. It pays no corporate income tax on the commission income it receives. This ensures there is no “double taxation” of profits; instead, earnings pass through to shareholders with maximum efficiency.

- Deductibility for the Exporter: Simultaneously, the commission paid to the IC-DISC is a fully deductible expense for the exporting business. This deduction reduces the exporter’s taxable income at the entity level, creating immediate tax relief.

- Combined Effect and Annual Savings: The combination of a business-level deduction and a lower shareholder-level tax rate can reduce federal tax liability by six figures or more, depending on your volume of qualified export income.

2026 Reality Check: Total savings are taxpayer-specific. Your actual benefit will depend on your total income level, state tax treatment, and the specific volume of income that meets the qualified export property requirements.

Example Calculation:

A U.S. exporter with $2 million in qualified export income might generate an IC-DISC commission of $1 million. By shifting that $1 million from a 37% ordinary rate to a 20% qualified dividend rate, the owners could realize $170,000 in federal tax savings in a single year.

To see how these variables apply to a business like yours, explore our detailed IC-DISC example case study.

Who Qualifies for IC-DISC? Eligibility Criteria for U.S. Exporters

While the tax benefits of the IC‑DISC are substantial, the IRS maintains strict compliance standards regarding who qualifies and how the structure is maintained. For the 2026 tax year, a wide range of U.S. businesses, including manufacturers, distributors, and architectural or engineering service providers, continue to leverage this incentive by meeting the following core requirements.

The Statutory Entity Tests

To be recognized as a valid IC-DISC, the entity must be a domestic C Corporation that satisfies the “95/95” tests and specific formation rules under Section 992.

- Domestic Corporation: Must be legally formed in the U.S.

- The 95% Gross Receipts Test: At least 95% of the entity’s gross receipts must be “qualified export receipts.”

- The 95% Assets Test: At least 95% of the entity’s assets (by adjusted basis) must be “qualified export assets” at the close of the taxable year.

- Capitalization & Stock: Must have at least $2,500 in par value or paid-in capital and maintain only one class of stock.

- Valid Election: The corporation must have a valid IC-DISC election in effect (Form 4876-A).

- Maintenance: The entity must maintain its own bank account and keep separate books and records.

The IC‑DISC can be owned by S Corporations, LLCs, partnerships, or individuals, providing immense flexibility for U.S. exporters without requiring a change to their primary operating structure.

Export Property & Foreign Use Requirements

For income to qualify for IC-DISC treatment, the underlying goods or services must meet the IC-DISC rules regarding content and destination:

- U.S. Content (The 50% Rule): The property must be manufactured, produced, grown, or extracted in the U.S., and at least 50% of its fair market value must be attributable to U.S. content.

- Foreign Use: Sales must be destined for use outside the United States. This includes Direct Exports (shipping to a foreign customer) and Indirect Exports (selling to a domestic customer who then exports the product).

Common Qualifying Goods: Machinery, medical devices, software incorporated into exported hardware, and agricultural products. Property that is merely imported and resold without significant domestic value-add does not qualify.

2026 Compliance Checklist

Before filing your Form 1120-IC-DISC this year, ensure you can answer “Yes” to these four pillars of eligibility:

- [ ] Entity Test: Is our election valid, and do we meet the 95/95 receipts and assets tests?

- [ ] Qualified Receipts: Have we scrubbed our sales data to confirm all included revenue meets the statutory definition of export receipts?

- [ ] Substantiation: Do we have documentation (shipping logs, certificates of foreign use) to support U.S. content and foreign destination?

- [ ] Operational Formalities: Are our separate books, dedicated bank account, and commission workpapers fully updated for the 2026 cycle?

For a deeper dive into how these rules apply to specific sectors, explore which industries can benefit from an IC-DISC.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Schedule Free ConsultationWhich Products and Services Qualify for IC-DISC?

To benefit from the IC-DISC incentive, your company must generate income from qualified export property or specific export-related services. In the current 2026 regulatory environment, the IRS maintains a rigorous “facts and circumstances” approach to qualification, anchored in the definitions found in 26 CFR § 1.993-1.

Tangible Products

Most physical goods manufactured, produced, grown, or extracted in the U.S. for foreign use will qualify, provided they meet the 50% U.S. content test. Common examples include:

- Industrial Goods: Machinery, equipment, and fabricated metal parts.

- Agriculture & Food: Processed food, agricultural commodities, and seafood.

- Technology: Electronics and medical devices.

Companies in manufacturing, distribution, and specialized industries frequently meet these criteria.

Software: Packaged vs. SaaS

The qualification of software remains a nuanced area of taxation for foreign income. While traditional SaaS (Software as a Service) and pure cloud downloads typically do not qualify as “export property,” software may be eligible when:

- It is embedded in exported hardware or equipment.

- It is sold as a licensed product on physical media for use abroad.

Export-Related Services

For the 2026 filing cycle, service providers must be particularly careful, as eligibility is strictly defined by statute. Services generally only qualify if they are “subsidiary and directly related” to a qualified export sale or fall into specific professional categories:

- Architectural & Engineering: Design and consultation for construction projects located outside the U.S.

- Technical Services: Support services related to the sale or lease of qualified export property.

Compliance Tip: Qualification for services depends heavily on the specific type of receipts and documented facts. Always consult the latest PLRs and the “Interest of Government Not Prejudiced” testto understand how the IRS evaluates complex service arrangements.

Indirect Exports (The “Supply Chain” Benefit)

You do not have to be the exporter of record to benefit. If you sell a U.S.-made component to a domestic customer who then incorporates it into a finished product and exports it, your sale may qualify. This requires maintaining documentation—such as a certificate of foreign use—to prove the product’s final destination.

What Doesn’t Qualify (2026 Red Flags)

To avoid audit triggers, ensure your IC-DISC commission does not include:

- Low U.S. Content: Products with less than 50% U.S. value-add.

- Domestic Use: Sales where the final destination or primary use is within the U.S.

- Non-Qualified Services: Most standalone consulting, legal, or financial services.

- Re-Exports: Foreign-made products that are simply moved through the U.S. without significant modification.

For broader export compliance standards beyond tax, you can visit the official U.S. export resource at Trade.gov.

How to Determine If Your Business Qualifies (2026 Action Plan)

If your company exports U.S.-made goods or provides eligible services linked to foreign projects, you likely have an opportunity to significantly reduce your tax liability. However, in the 2026 filing environment, determining eligibility is no longer just about “exporting”—it requires a structured verification process to bridge the gap between theory and actual tax savings.

To confirm your readiness, follow this six-step decision framework:

- Review Export Revenue: Analyze your gross receipts to ensure they meet the 95% qualified export receipts threshold.

- Identify Qualifying Categories: Determine which of your products or services align with IC-DISC rules (e.g., manufacturing vs. standalone services).

- Confirm U.S. Content: Verify that your products contain at least 50% U.S. content by fair market value.

- Audit Foreign Use Documentation: Ensure you have the necessary “foreign use” certificates or shipping logs to defend your claims.

- Model the Tax Benefit: Run a preliminary IC-DISC tax strategy model to estimate your net savings after implementation costs.

- Confirm Entity Readiness: Verify that your books, bank accounts, and corporate elections are properly structured to withstand IRS scrutiny.

Consulting with a specialist is the most effective way to maximize your IC-DISC while ensuring total compliance with the latest 2026 reporting standards.

How to Set Up an IC-DISC (and Stay Compliant)

Setting up an IC-DISC is a strategic move, but in 2026, precision is non-negotiable. While the structure is straightforward, the IRS requires strict adherence to corporate formalities and filing deadlines to preserve your tax benefits.

Here is the updated checklist for forming and maintaining a properly functioning IC-DISC in the current regulatory environment.

1. Form a Separate C Corporation

The IC-DISC must be a domestic C Corporation organized under U.S. law. To satisfy Section 992 requirements, it must:

- Maintain only one class of stock.

- Hold at least $2,500 of par value or paid-in capital on each day of the taxable year.

- Maintain a dedicated U.S. bank account and separate books and records.

- This entity typically has no employees or physical operations; it is a “shell” corporation sanctioned by the tax code for this specific purpose.

2. File IRS Form 4876-A (The Election)

To make the IC-DISC status official, you must file Form 4876-A.

- The Deadline: For new corporations, this must be filed within 90 days of the beginning of the first taxable year.

- The Stakes: This is a one-time election, but it is critical. If the form is missed or filed incorrectly, the IRS may deny all IC-DISC benefits for that year.

3. Draft and Sign a Commission Agreement

Your operating business must have a written, legally binding commission agreement with the IC-DISC. This document outlines the IC-DISC commission payment rules, specifying the calculation method used (e.g., 4% of gross receipts or 50% of export net income) and the documentation requirements to support those payments.

4. Calculate and Pay the Annual Commission

Each year, the operating business must calculate the commission using IRS-approved pricing methods.

- Compliance Tip: You must document exactly how the commission was derived.

- The Deadline: Under current IC-DISC commission payment due date rules, the commission must be paid within 60 days after the close of the IC-DISC’s taxable year to be considered a qualified asset.

5. File the IC-DISC Tax Return (Form 1120-IC-DISC)

Even though the entity is tax-exempt, filing is mandatory.

- Important 2026 Update: According to current IRS instructions, Form 1120-IC-DISC is due by the 15th day of the 9th month after the end of the tax year (e.g., September 15th for calendar-year entities).

- No Extensions: Unlike most corporate returns, no extensions are allowed for Form 1120-IC-DISC. Missing this deadline can jeopardize the entity’s status for the year.

6. Maintain Audit-Ready Documentation

To pass IRS scrutiny, you must keep detailed shareholder records and substantiation for every dollar of export income. This includes:

- Export Substantiation: Shipping logs, invoices, and certificates of foreign use.

- U.S. Content Support: Workpapers proving the 50% U.S. content requirement.

- Commission Support: Detailed 1120-IC-DISC instructions emphasize that your “Schedule P” calculations must be documented and supportable.

We help clients build audit-ready documentation tailored to their specific industry and export model to ensure their IC-DISC tax return is bulletproof.

Why Work with a Specialist?

While it’s possible to set up an IC-DISC internally, it’s easy to make mistakes that reduce or eliminate tax benefits. At Export Tax Management, we offer turnkey IC-DISC setup and compliance based on 25+ years of focused experience.

We handle:

- Entity formation and IRS filings

- Commission modeling and documentation

- Ongoing compliance, reporting, and support

Learn more about our IC-DISC implementation services

How IC-DISC Commissions Are Calculated (and Why It Matters)

At the heart of the IC-DISC structure is the commission payment from the exporting business to the IC-DISC entity. For the 2026 tax year, the IRS continues to allow these commissions to be calculated using specific “safe harbor” pricing methods under IRC Section 994. These methods are designed to encourage exports by allowing higher commissions than standard arm’s-length pricing might dictate.

The goal is simple: a higher allowable commission results in a larger tax deduction for the exporter and greater tax savings when those profits are distributed through the IC-DISC.

The Two Primary Pricing Methods

Under Treas. Reg. § 1.994-1, exporters typically choose between two main calculation strategies:

- 4% of Gross Receipts Method: The exporter pays a commission equal to 4% of qualified export gross receipts, plus 10% of any export promotion expenses. This is capped at 100% of the related taxable income. This method is often the go-to for high-volume, lower-margin exporters.

- 50% of Combined Taxable Income (CTI) Method: The commission equals 50% of the combined taxable income from qualifying export sales, plus 10% of export promotion expenses. This method considers actual profitability and is generally more beneficial for high-margin businesses, such as software or custom manufacturing firms.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Schedule Free ConsultationThe “Best-of-Both” Optimization

One of the most powerful features of the IC-DISC is the ability to optimize your IC-DISC commission calculation on a transaction-by-transaction basis or by grouping similar products.

By performing a “best-of-both” analysis, you can select the method that yields the highest deduction for every individual sale. In 2026, this level of granular analysis is essential for those looking to maximize their IC-DISC benefits.

Critical 2026 Compliance Factors

When finalizing your calculations for Schedule P (Form 1120-IC-DISC), keep these current regulatory constraints in mind:

- The “No-Loss” Rule: You must be careful not to trigger the IC-DISC no-loss rule, which generally prevents a commission from creating a net loss for the exporting company on a specific sale or group of sales.

- Marginal Costing: In certain scenarios where export sales are “marginal,” specialized costing rules can further increase the CTI and, consequently, the commission.

- Reporting Precision: Current IRS reporting requires that these calculations be finalized and documented by the time the return is filed. For a technical deep dive into these requirements, see our guide on understanding Treas. Reg. § 1.994-1(e)(3)(ii).

Example Scenario: 4% vs. 50%

Suppose a company earns $5 million in qualified export sales with $1.5 million in CTI from those sales.

| Method | Calculation | Potential Commission |

| 4% Method | $5,000,000 × 4% | $200,000 |

| 50% Method | $1,500,000 × 50% | $750,000 |

In this case, the 50% method is the clear winner, generating a significantly larger deduction.

Real-World Impact: The Savings Breakdown

Using the $750,000 commission from above, here is how the tax arbitrage works in practice:

- With No IC-DISC: $750,000 is taxed as ordinary income at 37% = $277,500 Tax

- With IC-DISC: $750,000 is deducted by the exporter and paid to shareholders as a dividend at 20% = $150,000 Tax

- Annual Net Savings: $127,500

By utilizing these statutory pricing methods, the business reduces its tax burden on export profits by over 45% without altering a single day-to-day operation.

Compliance and Reporting Requirements

Maintaining an IC-DISC requires strict adherence to federal reporting standards. The IRS revised its 1120-IC-DISC instructions in late 2025, and the finalized materials posted in early 2026 have clarified several critical filing protocols.

- Non-Negotiable Deadline: Form 1120-IC-DISC must be filed by the 15th day of the 9th month after the IC-DISC’s tax year ends (e.g., September 15th for calendar-year entities).

- No Extensions: Unlike standard corporate returns, the IRS does not allow extensions for the IC-DISC tax return. Missing this window can jeopardize the entity’s tax-exempt status for the year.

- Comprehensive Reporting: A valid filing must include Schedule P for intercompany pricing and commission calculations, as well as Schedule K for shareholder distributions.

- Documentation is Key: Poor documentation remains the primary driver of audit risk. You must maintain contemporaneous workpapers that support your qualified export receipts and U.S. content calculations.

Technical Resource: Review the official IRS instructions for Form 1120-IC-DISC to ensure your 2026 filing meets the latest criteria.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Schedule Free ConsultationPotential Risks & Challenges of IC-DISC

While the benefits are significant, exporters must navigate several practical challenges to maintain a compliant IC-DISC tax strategy:

- Audit Exposure: Increasing IRS scrutiny on “paper” entities requires robust audit-ready workpapers.

- Setup Failures: Failing to file Form 4876-A on time or neglecting the $2,500 capitalization rule.

- Substantiation Gaps: Weak support for qualified export receipts or failing the 50% U.S. content test.

- Commission Errors: Using incorrect pricing methods or missing the 60-day payment deadline.

State Tax Implications of IC-DISC

The federal tax-exempt status of an IC-DISC does not guarantee the same treatment at the state level. In 2026, state conformity remains a moving target:

- Planning: Proper international tax planning should account for where your shareholders reside, as this can impact the final state-level tax outcome.

- Varying Treatment: Some states follow federal rules (conforming), while others may tax the IC-DISC as a regular corporation or disallow the commission deduction.

- Annual Review: Because state laws change frequently, an annual state-by-state review is essential to avoid tax surprises.

IC-DISC vs. Other Export Tax Incentives

While the IC-DISC is one of the most valuable tax incentives available to U.S. exporters, it’s not the only one.

Other tax-saving strategies, such as the Foreign-Derived Intangible Income (FDII) deduction, can also provide benefits.

Understanding how the IC-DISC compares to these alternatives, and whether they can be used together—helps businesses optimize their tax savings.

1. How IC-DISC Compares to FDII (Foreign-Derived Intangible Income)

The FDII deduction was introduced as part of the 2017 Tax Cuts and Jobs Act (TCJA) to encourage U.S. companies to sell goods and services internationally. Unlike the Interest Charge Domestic International Sales Corporation, which is available to businesses of all sizes, FDII primarily benefits C corporations with foreign-derived income.

Here’s how they compare:

| Feature | IC-DISC | FDII Deduction |

| Who Can Use It? | Any business structure (C corps, S corps, LLCs, partnerships, individuals) | Only C corporations |

| Qualifying Income | Export sales of U.S.-made products & services | Foreign-derived intangible income (royalties, licensing, certain services) |

| Tax Benefit | Converts export income into lower-taxed qualified dividends | Reduces corporate tax rate on eligible foreign income to ~13% |

| Best For | Small to mid-sized exporters, manufacturers, distributors | Large multinational corporations |

For businesses that qualify, IC-DISC and FDII can sometimes be used together, allowing exporters to benefit from both incentives.

2. Can IC-DISC Be Used with Other Tax-Saving Strategies?

Yes! Many exporters combine the IC-DISC with other tax strategies to maximize savings. Common approaches include:

- Using IC-DISC with an S-Corp or LLC to pass through tax benefits to individual owners

- Combining IC-DISC with FDII for companies structured as C corporations

- Pairing IC-DISC with R&D tax credits for manufacturers investing in innovation

3. Which Export Tax Incentive Is Best for Your Business?

Choosing the right strategy depends on business structure, revenue, and long-term goals. While the IC-DISC remains the only statutory U.S. export tax incentive, businesses should consult with an experienced tax professional to determine if other strategies can further enhance tax savings.

How to Maximize IC-DISC Benefits

Setting up an IC-DISC is just the first step, maximizing its benefits requires careful tax planning and strategic structuring.

By optimizing commission calculations, aligning ownership structures, and working with an IC-DISC specialist, businesses can significantly enhance their tax savings.

1. Advanced Tax Planning Strategies

To fully leverage an IC-DISC, businesses should go beyond the basic setup and explore strategies such as:

- Optimizing commission calculations: Instead of defaulting to the 50% of net export income or 4% of gross sales method, businesses can conduct detailed transfer pricing studies to identify the most advantageous commission structure.

- Strategic dividend distributions: Timing distributions to shareholders can help minimize overall tax exposure, particularly if personal tax rates are expected to change.

- Using an IC-DISC as a wealth transfer tool: Business owners can gift shares of the IC-DISC to family members or trusts, allowing them to transfer wealth while taking advantage of lower tax rates on qualified dividends.

2. Structuring an IC-DISC for Maximum Savings

The ownership structure of an IC-DISC can have a significant impact on tax savings. Consider the following approaches:

- Owned by individual shareholders: Profits flow through as qualified dividends, taxed at a lower rate (15-20%) instead of ordinary income rates.

- Owned by a Roth IRA or trust: This structure can create long-term tax deferral benefits, as Roth IRAs are tax-free and trusts can be used for estate planning purposes.

- Owned by an ESOP (Employee Stock Ownership Plan): This allows employees to benefit from the IC-DISC tax savings while providing retirement benefits.

3. Why Working with an IC-DISC Specialist Is Crucial

While an IC-DISC can generate substantial tax savings, the rules surrounding commission calculations, compliance, and ownership structures can be complex.

A tax professional who specializes in IC-DISC strategies can help businesses:

- Ensure compliance with IRS regulations to avoid audits

- Optimize commission calculations for the highest possible tax savings

- Implement advanced tax strategies that align with long-term business goals

By taking a proactive approach, businesses can maximize the value of their IC-DISC, reduce their overall tax burden, and increase their financial flexibility for future growth.

FAQs: Quick Answers to Common IC-DISC Questions

Many business owners have questions about how an IC-DISC works, who can use it, and how quickly they can see tax savings. Below are answers to some of the most frequently asked questions.

To qualify for Interest Charge Domestic International Sales Corporation status, a company must generate at least 95% of its gross receipts from export sales, with at least 50% of the product’s value coming from U.S. content.

Yes! An IC-DISC can be owned by an S-corporation, LLC, partnership, or even individual shareholders. The tax savings still apply because the IC-DISC earns commissions from the operating company and distributes them as lower-taxed qualified dividends. However, an IC-DISC itself must be structured as a C-corporation to qualify for tax-exempt status.

No, an IC-DISC is not required to have employees, a physical office, or active operations. It is simply a tax-advantaged commission entity. However, it must exist as a separate legal corporation, maintain its own bank account, and follow IRS compliance rules.

Businesses typically see tax savings in their first year of operating an IC-DISC, as long as it is properly set up before the tax year begins. Once the commission payments are made, the operating company benefits from immediate tax deductions, and shareholders receive reduced-tax dividends.

An IC-DISC is flexible, if export sales vary from year to year, commissions and tax benefits will adjust accordingly. Even in lower export years, maintaining an IC-DISC ensures the structure is in place for future tax savings.

There is no specific minimum revenue required to set up an IC-DISC, but to make it worthwhile, a business should have at least $1 million in annual export sales. Companies with smaller export volumes may not generate enough tax savings to justify setup and maintenance costs.

To set up an IC-DISC, you must form a separate legal entity, complete IRS Form 4876-A, and meet other eligibility requirements.

IC-DISCs require extensive documentation, including tax returns, financial records, and records of export sales.

IC-DISC has remained stable, but periodic reviews with tax experts ensure you stay compliant and benefit from any updates

Do You Have More Questions About IC-DISCs?

If you still have questions about IC-DISCs or need assistance determining if it’s the right strategy for your business, Export Tax Management is here to help. Our experts can provide tailored guidance and support throughout the IC-DISC process. Contact us today to schedule a consultation and explore how an Interest Charge Domestic International Sales Corporation can optimize your export strategy. Or take a look at our FAQs video:

Conclusion & Next Steps

The IC-DISC remains one of the most valuable tax incentives for exporters, offering a permanent reduction in federal tax liability. However, the 2026 landscape demands higher standards for documentation, reporting, and strategic modeling.

Actual savings depend on your unique export profile, ownership structure, and meticulous adherence to the 95/95 asset and revenue tests.

Ready to optimize? Don’t leave export savings on the table. Contact us today for a consultation and discover how much your business could save.