Taxpayers utilizing an IC-DIS should note the continuing importance of Schedules K-2 and K-3 in reporting international income. Since 2022, S corporations and partnerships receiving IC-DISC dividends must include this information to comply with the requirements of Schedule K-2/K-3.

Although IC-DISCs are domestic entities (Treas. Reg. § 1.992-1(a)(1)), dividends paid by an IC-DISC are classified as foreign-source income under Treas. Reg. § 1.904-4(b)(3) and Rev. Rul. 73-68. These dividends fall under the ‘specified passive category’ for foreign tax credit purposes.

If your IC-DISC is owned by an S corporation or partnership, be sure to reflect the foreign-source nature of the dividends on Schedules K-2 and K-3 to avoid potential issues with the IRS.

The IRS’s expanded international reporting requirements have made it essential for S corporations and partnerships with IC-DISCs to understand how to properly report dividends on Form Schedule K-2/K-3. Below is a summary of key developments that may affect Forms 1120S or 1065.

1. Schedule K-2/K-3 Applies to Pass-Through Entities with International Activity

Effective in 2022, both partnerships and S corporations must file Schedule K-2 and K-3 if they have international tax items.

These forms report details on foreign-source income, foreign taxes paid, and calculations for the foreign tax credit (FTC).

Incomplete or incorrect filings can delay partner/shareholder tax returns and compromise the ability to fully utilize a FTC.

2. IC-DISC Dividends in a Pass-Through Structure

Many exporters utilize an S corporation or partnership as the parent entity of an IC-DISC.

The IC-DISC pays qualified dividends to the parent entity, which then distributes that income to shareholders or partners through Schedule K-1.

3. Foreign-Source Nature of IC-DISC Dividends

While an IC-DISC must be incorporated in the U.S. under Treas. Reg. § 1.992-1(a)(1), its dividends are treated as foreign-source income.

Under Rev. Rul. 73-68 and Treas. Reg. § 1.904-4(b)(3), these dividends are classified as “specified passive category” foreign income for FTC purposes.

This distinction can be easily overlooked but has important implications for proper FTC reporting and sourcing rules.

4. Key Reporting Considerations for Schedule K-2/K-3

When preparing Schedules K-2 and K-3:

Include the dividend income in Part II of Schedule K-2 and pass it through to Schedule K-3.

Source the income as foreign, not domestic, despite the IC-DISC being a U.S. entity.

Classify it as specified passive category income for FTC limitation purposes.

Accurate reporting helps shareholders claim FTCs.

What You Should Do Now

Review your IC-DISC structure and whether your entity’s dividends are properly sourced.

Ensure that your tax preparers and advisors are familiar with the nuances of IC-DISC and K-2/K-3 reporting.

https://www.exporttaxmanagement.com/wp-content/uploads/2025/06/Update-on-the-IC-DISC.jpg500800Paul Ferreirahttps://www.exporttaxmanagement.com/wp-content/uploads/2024/03/Export-Tax-Management-Black-Logo.pngPaul Ferreira2025-06-23 13:58:002025-06-24 14:08:36Update on the IC-DISC – Schedule K-2/K-3 and the IC-DISC Dividend

Export-driven tax breaks give U.S. companies a powerful way to keep more of every overseas sale.

The primary US-based tax incentives for exporters are the Interest Charge Domestic International Sales Corporation (IC-DISC) and Foreign Derived Intangible Income (FDII). An IC-DISC is a separately formed business entity that makes a commission on certain export sales. The federal tax rates are lower when those payments are distributed as qualified dividends.

This guide to export incentives will explain your options in more detail, the expected tax benefits and other advantages, and how to begin reaping tax savings.

What Are Export Incentives?

Export incentives are government-backed tools — usually created by statute or regulation — that lower the cost or raise the after-tax profit of selling U.S. goods or services abroad.

They come in four main flavors:

Tax-based

IC-DISC (Interest-Charge Domestic International Sales Corporation)

FDII (Foreign-Derived Intangible Income)

What they do: Reduce federal income tax on qualifying export earnings

Financing & Insurance

Export-Import Bank loan guarantees

SBA Export Express loans

What they do: Cut borrowing costs and transfer credit risk

Direct Grants & Promotion

USDA Market Access Program

Commerce trade missions and matchmaking grants

What they do: Offset marketing expenses and open doors to foreign buyers

Tariff & Duty Relief

Duty Drawback

Foreign-Trade Zones

What they do: Eliminate or defer customs duties on inputs destined for re-export

Together, these programs encourage U.S. companies to enter or expand in overseas markets by improving cash flow, reducing risk, and sharpening price competitiveness.

How Export Incentives Work

In the United States, export incentives operate by lowering the cost and risk of selling abroad, thereby helping U.S. goods and services compete more effectively in foreign markets. They do this through four broad channels:

Tax-based incentives – The Interest-Charge Domestic International Sales Corporation (IC-DISC) structure lets qualifying exporters treat a portion of export profits as qualified dividends, generally taxed at a lower rate than ordinary income. This effectively boosts after-tax margins on foreign sales.

Customs relief – Programs such as duty drawback and Foreign-Trade Zones (FTZs) refund or eliminate U.S. import duties on inputs that are later re-exported, trimming the landed cost of finished products.

Export financing and risk mitigation – The Export–Import Bank of the United States (EXIM) provides loan guarantees, direct loans, and export credit insurance, while the USDA’s GSM-102 guarantees help agricultural exporters. These tools substitute the federal government’s credit rating for that of the exporter or buyer, making overseas deals easier to finance and insure.

Cost-sharing grants and advisory support – Programs like the Small Business Administration’s State Trade Expansion Program (STEP) and the Commerce Department’s International Trade Administration (ITA) reimburse part of the expense of trade shows, market research, and compliance, and offer technical guidance on foreign regulations.

Export Tax Management Inc. specializes in IC-DISC incorporation, compliance, and implementation. Explore your tax incentive options with our services.

Export Incentives and the World Trade Organization (WTO)

According to the International Trade Administration, the US already exports $2 trillion in services and goods worldwide but can always afford to expand.

That’s why Congress created the IC-DISC in 1971. That’s not the only tax incentive for US corporations with foreign presences; FDII is another popular option.

Export Tax Management Inc. specializes in IC-DISC incorporation, compliance, and implementation. Explore your tax incentive options with our services.

Program

WTO compliance status (as of May 2025)

Why this is the right label

IC-DISC

Likely compliant (never challenged)

No WTO member has ever brought a case; commentators note it sidesteps the “export-contingent” test because the tax benefit applies only after income exists and without volume triggers. (Capstone Associated)

FDII deduction

Unchallenged — under scrutiny

EU letter (2019) signals a possible WTO complaint, arguing the deduction is tied to foreign sales, but no dispute has been filed to date.

Foreign Sales Corporation (FSC) — repealed

Prohibited

Panel/Appellate Body found FSC to be an export-contingent tax subsidy (DS108, 2000). (Trade and Economic Security)

Extraterritorial Income (ETI) — repealed

Prohibited

FSC replacement (ETI Act) was also ruled WTO-inconsistent in 2002 and again in 2006 compliance proceedings. (Trade and Economic Security)

USDA GSM-102 export-credit guarantees (pre-2014)

Prohibited

GSM-102, GSM-103 and SCGP guarantees for cotton and other products were condemned as export subsidies in DS267 (Brazil v. U.S.). (Every CRS Report)

USDA GSM-102 (post-2014 reforms)

Generally compliant

2014 U.S.–Brazil settlement added higher fees and shorter tenors; Brazil dropped retaliation and pledged no new WTO action while the program follows the agreed terms. No new disputes have been filed. (USDA)

Quick Rule of Thumb

Safe: Tax deductions or grants you can claim whether or not you hit an export target—e.g., IC-DISC, FDII, R&D credits, FTZ duty savings.

At Risk: Any cash, credit guarantee, or lower tax rate you receive only because the product is exported (and that scales with export volume or price). Those features invited—and lost—the FSC/ETI and Cotton cases.

The Types of Tax Incentives for Exporters in the USA

Here’s an overview of the tax incentives exporters can take advantage of:

U.S. Tax Incentives Exporters Can Use

Tool

Typical Eligibility Test

How the Benefit Works

Export-Relevant Example

Tax Credit

Activity must satisfy a statutory purpose (e.g., R&D, renewable energy, hiring veterans).

Reduces tax liability dollar-for-dollar. Some credits are non-refundable (only offset tax owed); others are refundable (excess is paid out).

• Research & Experimentation Credit for product improvements sold abroad. • Foreign Tax Credit for income taxes already paid to a foreign government.

Tax Deduction

Expense must be ordinary and necessary to the business (IRC §162) or specifically listed in the Code.

• IC-DISC commission deduction (see below). • FDII deduction on profits from serving foreign markets. • Standard deductions for travel, marketing, insurance, etc. tied to export sales.

Tax Exemption / Exclusion

Income type is expressly carved out from tax base.

Income is never taxed, so benefit is 100 % of the amount excluded.

• Interest on certain state or municipal export-finance bonds (federal exemption). • State-level sales-tax exemptions for goods shipped abroad.

Where Does IC-DISC Fit?

Step

Tax Treatment

Effect

1. Exporter pays an IC-DISC “commission.”

Exporter deducts the commission as an ordinary business expense.

Deduction reduces exporter’s taxable income.

2. Commission is retained inside the IC-DISC.

IC-DISC itself is not taxed on the income it earns.

Functionally an exemption at the entity level.

3. IC-DISC distributes profits to its shareholders.

Shareholders receive qualified dividends (2025 top rate: 20 % + NIIT) instead of ordinary income.

Converts export profit into lower-rate income—often described as a tax-favored dividend.

Tax credits allow taxpayers to deduct a specific amount by the dollar from their federal income taxes. Businesses pay less money on their taxes as a result. Tax credits can be partially refundable, fully refundable, or nonrefundable.

A refundable or partially refundable tax credit generates a refund according to the prescribed amount. States and the federal government will make tax credits available to qualifying businesses.

Tax Deductions

Another type of tax incentive exporters should consider is a tax deduction. Businesses can subtract a sum from their taxable income, paying less on their taxes. Types of deductions include itemized or standard deductions.

You subtract the amount due by taxable income, and thanks to The Tax Cuts and Jobs Act, the amount of standard deductions is higher than ever

Some deductions small businesses and startups are eligible to claim on their tax returns are as follows:

Startup expenses

Vehicle costs

Property, sales, and local taxes

Maintenance and repairs

Pass-through tax deductions

Loan interest

Regulatory and licensing fees

Professional and legal fees

Insurance

Equipment

Bad debts

Marketing and advertising

Business travel

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Exporters should also consider their tax exemption eligibility. A tax exemption reduces the corporation’s tax obligation. Municipal, county, and state governments offer exemptions.

IC-DISCs and other tax-exempt organizations can also reduce their federal income tax rate.

Tax incentives share many similarities in how they reduce a corporation’s taxes owed. However, the different ways incentives lower taxes and the eligibility criteria make it worth a corporation’s time to thoroughly explore deductions versus credits versus exemptions, especially as they apply to IC-DISC and FDII.

Learn more about the differences between these two tax incentives for exporters in our article.

Want to explore how tax exemptions and incentives like IC-DISC can benefit your business?

At Export Tax Management Advisory Firm, we specialize in IC-DISC and can help you navigate exemptions, deductions, and credits to maximize your tax savings and boost your bottom line. Reach out to us for a consultation today!

Why the IC-DISC Is the Best Choice as a Tax Incentive

IC-DISC stands head and shoulders over FDII and other tax incentives for exporters eager to claim more tax savings. An IC-DISC is a Congress-issued tax incentive and tax code that broadens the scope of US sales in foreign countries and opens the door to exporting.

Eligible companies must establish an IC-DISC separate from their main entity, with it operating as a tax-exempt entity without office space or employees. The exporter or shareholders must form the IC-DISC, with a required delineation between it and C corporations.

When the corporation makes an international sale, it owes the IC-DISC a commission. The commission is deductible as a business expense. No federal income taxes are owed until the IC-DISC begins paying owner dividends.

The dividends have a tax rate of only 23.8 percent.

When should a corporation consider applying for IC-DISC status? Seek this tax benefit if a high tax rate has impeded business growth. Export Tax Management Inc. can help you determine the right road to tax savings and incentives for your business.

According to Schedules C and E of IRS Tax Form 1120, qualifying corporations can make the following deductions:

Freight insurance and freight

Contributions

Interest

Licenses and taxes

Bad debts

Employee benefit programs

Profit-sharing plans and pensions

Maintenance and repairs

Officer compensation

Warehousing

Sales commissions

Rent

Wages and salaries

Advertising and market studies

Nonqualified inclusions and dividends

Qualified dividends

Total inclusions and dividends

IC-DISC dividends (including former DISCs)

Global Intangible Low-Taxed Income or GILTI

Inclusions from controlled foreign corporation sales, in which a lower-tier foreign corporation’s stock was sold

Dividends from foreign sources where the foreign corporation owns at least 10 percent but is not a hybrid corporation

Dividends from wholly-owned foreign subsidiaries

Dividends from foreign corporations with less than, equal to, or more than 20 percent owned

Dividends on certain preferred stocks from public utilities that are less than or more than 20 percent owned

Dividends from foreign or domestic corporation debt-financed stock

Dividends from foreign corporations that are less than or more than 20 percent owned outside of debt-financed stock

Maximizing your IC-DISC is simple with the right support, such as from Export Tax Management Inc. For example, a bakery that produces goods in the US but sells them internationally would qualify for IC-DISC status, lessening its tax burden.

Advantages of Joining the IC-DISC Tax Incentives for Exporters

Delaying Taxes by Waiting to Pay Dividends on the Commission

While corporations under DISC status must still file taxes within nine months from the end of their tax year and by no later than the 15th day (unless that day falls on a weekend or holiday), when the corporation has to pay taxes under this tax incentive isn’t always the same.

A corporation can wait until it generates $10 million of export sales before paying the commission as a dividend. This limit resets every year.

Spending Less Money on Taxes

Corporations don’t want to spend more than necessary on their taxes, as the loss in capital can trickle down to other parts of the company. A bad tax year might cause a corporation to tighten its belt, reduce staff, or make other changes to stay in the green.

Tax incentives for exporters can reduce their federal income tax spending, preventing the above cost-cutting measures from transpiring. IC-DISC corporations can deduct up to 50 percent of export income.

Increasing a Corporation’s Income

A corporation will have more income after delaying dividends on commissions and reducing federal income tax spending. This wealth can be used to reduce costs, expand (such as hiring more staff or opening more offices and warehouses), and research and develop new products and services.

Expanding Business Internationally

The additional income and ability to continue expanding its roster of goods and services will allow DISC-qualifying corporations to expand business internationally, increasing export revenue.

Exporting goods from the United States to other parts of the world gives businesses a competitive advantage, reduces risk (other economies might fluctuate less than their home economy), and increases access to tax incentives.

Requirements to Enjoy the IC-DISC Tax Incentives for Exporters

Corporations applying for tax-exempt status must understand the eligibility requirements for export tax incentives.

Here are the eligibility criteria an IC-DISC must meet:

Up to 95 percent of its gross receipts must be qualified gross receipts.

It must pass an export assets and gross receipts test.

It must have only one stock class valued at $2,500 or higher.

It must have separate records from other business entities.

When adjusted, its qualified export assets must be worth 95 percent (or more) of its asset sums.

Qualifying corporations must document all income and spending, including dividends, deductions, special deductions, inclusions, and gross income, even if the corporation doesn’t pay taxes thanks to its tax-exempt status.

The corporation must also file taxes by the required deadline. Avoid common mistakes, such as failing to meet IC-DISC status yet filing as one anyway, skipping or leaving off important parts of Tax Form 1120, and failing to check your math before filing.

Where Do Most U.S. Exports Go?

Most U.S. exports go to Canada and Mexico, followed by China, Japan, and the United Kingdom. In 2022, these top five destinations accounted for a significant portion of total U.S. goods exports.

Canada: $356.5 billion (17.3% of total U.S. exports)

Mexico: $324.3 billion (15.7% of total U.S. exports)

China: $150.4 billion (7.3% of total U.S. exports)

Japan: $80.2 billion (3.9% of total U.S. exports)

United Kingdom: $76.2 billion (3.7% of total U.S. exports)

Other notable export destinations include: the European Union (27 countries) with a total of $350.8 billion in U.S. goods exports.

What Does the United States Export the Most?

The latest U.S. Census Bureau data for 2024 show that American exporters rang up a record $2.06 trillion in goods shipments. Five products alone accounted for more than a quarter of that total:

Rank

Leading export (2024)

Export value

Share of total U.S. goods exports

Major destinations

1

Civilian aircraft parts

$123 billion

6.0 %

France, Germany, Brazil

2

Crude oil

$118 billion

5.7 %

Netherlands, South Korea, Canada

3

Gasoline & other refined fuels

$118 billion

5.7 %

Mexico, Canada, Netherlands

4

Low-value shipments*

$68.2 billion

3 – 4 % (approx.)

Mexico, Canada

5

Liquefied natural gas (LNG) & other petroleum gases

$62.2 billion

3.0 %

Japan, Mexico, United Kingdom

Don’t forget services. Travel, business & professional services, telecom/IT services, and financial services together topped $1.1 trillion in 2024, with travel alone up $26 billion from 2023 .

Why Are Export Subsidies Considered Harmful?

Short answer: Because they distort prices, drain public budgets, and spark trade retaliation—often running afoul of WTO rules in the process.

Export-contingent subsidies offer short-term gains to a narrow group but impose long-term costs on the wider economy and trading partners.

WTO rules leave room for non-contingent support (e.g., general R&D credits, broad tax-rate reductions like IC-DISC), but programs that pay because you export invite litigation and retaliation.

For firms, the safest path is to use WTO-compliant incentives—lower tax rates on income already earned, duty-drawback on imported inputs, or neutral finance tools—rather than volume-linked rebates that can be challenged as prohibited export subsidies.

FAQs About Tax Incentives for Exporters

I. What is an exporter tax credit?

An exporter tax credit is a government incentive that lets a firm subtract a percentage of its qualified export earnings from the income tax it owes. The goal is to boost the price competitiveness of domestically made goods and services abroad.

II. Who qualifies for tax incentives?

Companies that earn a defined share of revenue from foreign sales and file the required export documentation generally qualify, with many programs also extending benefits to small or indirect exporters that supply exporters.

III. Are exports allowed to be taxed?

Most countries zero-rate or exempt exports from VAT or sales tax, and many prohibit export duties under trade agreements. A government may still levy an export tax in limited circumstances—such as on raw commodities for revenue or supply-security reasons—so long as it stays within its WTO commitments.

IV. What is Foreign-Derived Intangible Income (FDII), and how does it benefit exporters?

FDII is income from exporting intangible assets, such as patents, trademarks, or intellectual property. Exporters benefit from FDII through a reduced tax rate, effectively encouraging innovation and U.S.-based companies to sell their intangible assets in foreign markets while lowering their overall tax burden.

V. Can service companies qualify for export tax incentives?

Yes, certain service companies can qualify for export tax incentives, particularly if their services are related to foreign projects. Engineering, architectural, and software development firms that deliver services abroad can benefit from IC-DISC tax advantages, provided they meet the necessary qualifications.

Do you have more questions?

If you’re interested in learning more about tax incentives for exporters, Export Tax Management is ready to assist. For further information, explore our IC-DISC FAQs or contact us to schedule a consultation and discover how IC-DISC can boost your export tax savings strategy.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Book a Consultation Now to Maximize Your Tax Incentives

Tax incentives for exporters, like FDII and IC-DISC, offer powerful opportunities for businesses to reduce their tax burden and boost profitability. These incentives reward your efforts and position your company for global expansion.

In today’s complex tax environment, the DISC tax structure continues to be a critical tool for U.S. exporters aiming to stay competitive in global markets.

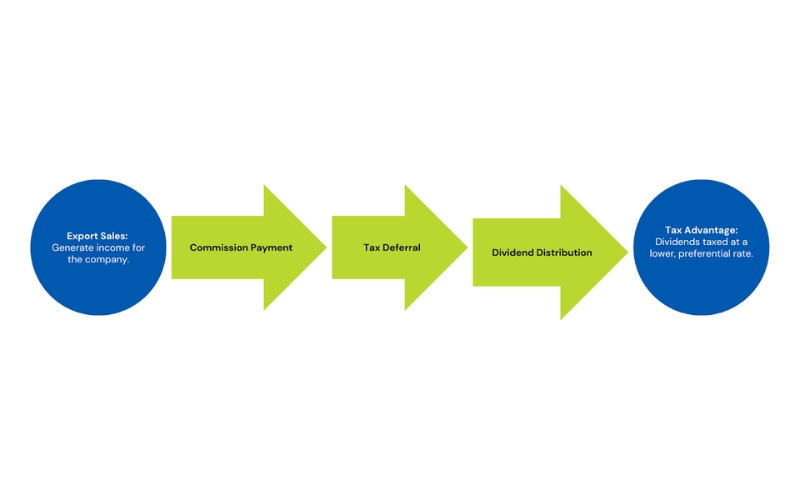

For U.S. companies that export products or services, the Interest Charge Domestic International Sales Corporation (IC-DISC) remains a powerful and often underutilized federal income tax incentive. By implementing the right IC-DISC structure, eligible businesses can significantly reduce the tax burden associated with export income—leading to meaningful savings and improved cash flow.

The IC-DISC structure operates within a specialized legal and organizational framework established by U.S. tax law to incentivize export activity.

A DISC must be a domestic corporation with a single class of stock and is required to elect DISC status by filing IRS Form 4876-A. The Interest Charge Domestic International Sales Corporation (IC-DISC) does not engage in active business operations but exists to receive commissions on export sales from the related operating company. This structure allows exporters to legally shift a portion of their profits into a tax-advantaged entity, benefiting from lower dividend tax rates. Closely-held and family-owned businesses frequently adopt this model to maximize tax efficiency.

For assistance with setting up a compliant DISC entity and other export tax solutions, visit ourExport Tax Services page. To explore official tax guidelines, visit the IRS website.

Qualification Requirements for IC-DISC Status

To fully utilize the DISC tax structure, a business must satisfy stringent IRS qualification criteria.

The Interest Charge Domestic International Sales Corporation (IC-DISC) must be a U.S.-incorporated entity with only one class of stock and properly elect DISC status. A key requirement is that at least 95% of the DISC’s gross receipts must come from qualified export property — goods produced in the U.S. and sold for use outside the country. Furthermore, companies must maintain precise documentation, separate books, and submit accurate annual filings such as Form 1120-IC-DISC. Ensuring compliance with these standards is crucial to preserving the DISC’s tax benefits and avoiding IRS challenges.

Operational Structure: How a DISC Functions in Practice

Understanding how the DISC tax structure operates in practice is essential for exporters looking to maximize its benefits.

The IC-DISC earns commissions from the related exporting company based on qualified export sales. These commissions are deductible expenses for the exporter and are taxed at favorable dividend rates when distributed to DISC shareholders. Typically, the transaction flow involves calculating commissions, transferring funds to the DISC, and adhering to strict payment timing rules. Exporters must follow specific guidelines regarding commission payments to remain compliant and ensure optimal tax treatment.

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

The DISC tax structure offers exporters a unique opportunity to enhance profitability while maintaining compliance with U.S. tax laws. Key advantages include:

Significant tax savings by converting ordinary income into qualified dividend income, taxed at lower rates.

Tax deferral opportunities, allowing businesses to postpone tax payments on export profits.

Improved cash flow, giving exporters more resources to reinvest in business growth.

Strategic planning benefits for family-owned and closely-held businesses, including succession and estate planning.

Simplicity and flexibility—the DISC structure does not require operational changes to the core business.

To explore these benefits in detail, visit our comprehensive guide on IC-DISC benefits. If you’re ready to implement or optimize your DISC strategy, learn more about our Export Tax Services.

Case Study: Real-World Application of the DISC Tax Structure

To illustrate the tangible benefits of the DISC tax structure, let’s look at a real-world example of a U.S.-based manufacturer leveraging an IC-DISC for export tax savings. This family-owned company produces specialized industrial equipment and exports a significant portion of its products to international markets.

Challenge: Despite steady growth in exports, the company faced high federal income tax liabilities, reducing overall profitability and limiting cash flow for reinvestment.

Solution: By establishing an Interest Charge Domestic International Sales Corporation (IC-DISC), the company was able to:

Pay commissions to the DISC based on qualified export sales.

Deduct these commissions from its taxable income.

Distribute the DISC’s income to shareholders as qualified dividends taxed at a lower rate.

Result: The IC-DISC resulted in:

Annual federal tax savings exceeding $500,000.

Improved cash flow, which was reinvested into R&D and global expansion.

Enhanced long-term financial planning for the company’s shareholders.

This case highlights how strategic use of the DISC tax structure can provide substantial tax relief and support business growth. For more practical examples of IC-DISC in action, visit our detailed IC-DISC Example page.

Frequently Asked Questions (FAQs)

I. What is a DISC in accounting?

A DISC (Domestic International Sales Corporation) is a U.S. tax-exempt entity that allows exporters to reduce their tax liability on profits from qualified export sales. From an accounting perspective, a DISC functions as a separate legal entity that receives commissions from the operating company. These commissions are deductible for the exporter and generate income for the DISC, which is then taxed at the favorable qualified dividend rate when distributed to shareholders.

II. What is an IC-DISC tax and how does it work?

The IC-DISC enables U.S. exporters to create a tax-exempt corporation that receives commissions based on export sales. The exporter deducts these commissions as an expense, reducing taxable income. Meanwhile, the IC-DISC’s income is taxed to shareholders at the lower qualified dividend rate, resulting in significant federal tax savings without altering the exporter’s core operations.

III. How is the IC-DISC commission calculated?

IC-DISC commissions are calculated using the greater of two methods:

– 4% of qualified export receipts, or

– 50% of export net income Exporters can choose the method that yields the highest commission benefit. Proper calculation is essential to maximize savings and comply with IRS rules.

IV. What is a practical example of an IC-DISC in use?

A typical example involves a U.S. manufacturer exporting machinery abroad. By setting up an IC-DISC, the company pays deductible commissions to the DISC based on its export sales. The DISC’s income is later distributed to shareholders as qualified dividends, effectively lowering the overall tax rate on those profits.

V. Is the IC-DISC still relevant under current tax laws?

Yes, despite changes in tax legislation, the IC-DISC remains the only statutory export incentive available today. It continues to provide substantial tax benefits for qualifying U.S. exporters, especially for closely-held businesses looking to reduce tax liabilities on export profits.

For more in-depth answers to these and other questions, be sure to visit our complete IC-DISC FAQ page.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Leveraging the DISC Tax Structure for Long-Term Success

The DISC tax structure remains one of the most effective export tax incentives for U.S. businesses seeking to reduce their federal tax liabilities and enhance international competitiveness. By channeling export profits through an IC-DISC, companies benefit from lower tax rates, improved cash flow, and strategic financial advantages—all while staying fully compliant with U.S. tax laws.

However, the true value of an IC-DISC lies in its proper setup, management, and alignment with your business goals. Partnering with experienced professionals ensures that you maximize these benefits without falling into compliance traps. If you’re ready to explore how your company can benefit, schedule a consultation with our experts.

For a full overview of how we support exporters with IC-DISC and other tax-saving strategies, visit ourExport Tax Services page.

https://www.exporttaxmanagement.com/wp-content/uploads/2025/05/DISC-Tax-Structure.jpg500800Paul Ferreirahttps://www.exporttaxmanagement.com/wp-content/uploads/2024/03/Export-Tax-Management-Black-Logo.pngPaul Ferreira2025-05-19 09:23:572025-05-19 09:24:01How an IC-DISC Structure Can Lower Federal Taxes on Export Income

The Interest Charge Domestic International Sales Corporation (IC-DISC) is the last surviving federal tax incentive specifically designed to promote U.S. export sales. Established by Congress in 1971, the IC-DISC provides substantial federal income tax savings — but only when businesses strictly follow IC-DISC rules.

IC-DISC rules are the legal requirements companies must meet to form, operate, and maintain a qualified IC-DISC entity under the Internal Revenue Code. These standards cover eligibility, formation procedures, operational guidelines, documentation, and annual tax reporting.

Navigating IC-DISC compliance can seem complex, but understanding the process is critical to maximizing benefits and avoiding costly mistakes.

In this guide, we explain formation and operational requirements, common pitfalls, and why working with an expert matters. Whether setting up a new IC-DISC or managing an existing one, mastering the rules is essential for success.

To learn more about how an IC-DISC works, visit our complete guide on IC-DISC Explained. You can also explore real-world scenarios on our IC-DISC Example page.

Formation Rules and Requirements

Establishing a compliant IC-DISC entity requires careful attention to formation rules, as even small mistakes can disqualify a business from receiving valuable tax benefits. Exporters must follow a specific process to ensure the corporation meets all regulatory standards from the beginning.

First, the IC-DISC must be created as a domestic C-Corporation under U.S. state law. It cannot be a partnership, sole proprietorship, or disregarded entity. The entity must maintain a separate legal existence distinct from its parent or operating company.

A critical step is filing the Form 4876-A (Election to Be Treated as an IC-DISC) within 90 days of the corporation’s formation. Missing this filing deadline can delay eligibility for an entire tax year. You can find official instructions for Form 4876-A directly from the IRS website.

In addition, an IC-DISC must maintain a minimum capitalization of $2,500 in authorized and issued shares. This requirement must be continuously met, as failure to maintain proper capitalization could jeopardize the corporation’s IC-DISC status.

Shareholder considerations are also essential. Ownership and distribution planning should account for the tax treatment of dividends and the potential impact on individual or corporate tax returns. For further guidance on the setup and compliance process, visit our resource on IC-DISC Management.

Failure to adhere to IC-DISC formation regulations can result in significant penalties or a loss of the tax benefits altogether.

Pro Tip: Missing the 90-day election window could cost a company an entire year’s worth of tax savings.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Once the IC-DISC entity is properly established, maintaining compliance with the applicable IC-DISC rules is essential. These regulations govern how the corporation must operate to retain its tax-advantaged status and avoid costly disqualification.

Below, we detail the primary operational standards that every IC-DISC must follow.

Qualified Export Receipts

An IC-DISC must derive at least 95% of its gross receipts from qualified export sales. “Qualified export receipts” include proceeds from the sale, lease, or rental of property manufactured, produced, grown, or extracted within the United States for direct use outside the country.

Examples of qualifying transactions include:

Sale of U.S.-made machinery to foreign buyers.

Engineering services for construction projects abroad.

Receipts that do not qualify include domestic sales and sales between related U.S. entities where no foreign use is involved. Businesses must carefully document each export transaction to verify compliance.

External reference: The IRS IC-DISC Audit Techniques Guide offers insight into how auditors review qualified receipts.

Qualified Export Assets

An IC-DISC must also maintain at least 95% of its assets as qualified export assets. These typically include:

Receivables from qualifying export transactions.

Export property inventories.

Temporary investments (if proceeds stem from export income).

If a corporation falls below the asset threshold, it risks disqualification under the strict IC-DISC compliance framework.

External support: For official asset qualification rules, review the U.S. Code § 992 outlining IC-DISC asset requirements.

Recordkeeping and Documentation

Strong internal documentation is crucial. Businesses must:

Maintain separate books and records for the IC-DISC.

Clearly document export transactions.

Track commission payments and ensure they relate to qualifying sales.

Maintaining organized, complete records protects the company during an IRS examination. To better understand this process, explore our page on IC-DISC Tax Return.

Annual Tax Filings and Reporting

Every IC-DISC must file an annual Form 1120-IC-DISC with the IRS. The filing deadline matches the 15th day of the 9th month after the end of the corporation’s tax year.

Key points:

Failure to file Form 1120-IC-DISC on time may result in penalties.

Annual distribution of commission income to shareholders must also comply with timing requirements.

Adhering to these core IC-DISC rules ensures your corporation remains in good standing and continues delivering significant federal tax benefits.

Who Can Qualify for an IC-DISC?

Qualifying for an Interest Charge Domestic International Sales Corporation (IC-DISC) requires meeting specific eligibility standards set by the IRS. According to IC-DISC rules, only certain types of businesses and products are eligible to take advantage of this powerful export tax incentive.

To form an IC-DISC, the entity must be a C-Corporation organized under U.S. law. This can include companies structured as Corporations, S-Corporations, LLCs (electing C-Corp tax treatment), Partnerships, or even individual-owned businesses willing to establish a new C-Corporation for the IC-DISC.

The business must sell products that are:

Manufactured, produced, grown, or extracted in the United States; and

Sold for direct use, consumption, or resale outside of the U.S.

Additionally, under the “50% U.S. content rule,” at least half of the product’s fair market value must come from U.S.-sourced materials, labor, or production costs. Export-related services like architectural, engineering, and construction services for foreign projects may also qualify under specific circumstances.

Choosing the right structure at the start is critical to ensuring a compliant and effective IC-DISC setup.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

While the Interest Charge Domestic International Sales Corporation (IC-DISC) structure offers outstanding tax benefits, failing to follow the proper IC-DISC rules can easily lead to disqualification, missed savings, or even IRS penalties. Many exporters unknowingly make mistakes that could be avoided with careful planning and ongoing compliance reviews.

Some of the most common IC-DISC mistakes include:

Improper Entity Formation: Failing to establish the IC-DISC as a valid C-Corporation or missing the critical 90-day election deadline can render the entity invalid for the entire year. Learn more about how to set up correctly in our resource on IC-DISC Management.

Inadequate Recordkeeping: Poor documentation of export sales, receipts, and commission payments is a major red flag during IRS audits.

Misclassification of Qualified Receipts or Assets: Incorrectly including domestic sales or improperly categorizing assets can cause the IC-DISC to fail the 95% qualification tests.

Neglecting Ongoing Compliance: Even after formation, regular maintenance is crucial. Many businesses make the mistake of assuming the IC-DISC is “set it and forget it.”

To avoid these pitfalls, the IRS provides guidance in its IC-DISC Audit Techniques Guide, which outlines key areas of risk.

Quick Tip: Regular audits and working with an experienced IC-DISC specialist can prevent expensive mistakes and ensure your company remains compliant year after year.

Why Work with an IC-DISC Specialist?

Navigating the intricate world of IC-DISC rules is not something most companies can—or should—attempt alone. The process of forming, maintaining, and optimizing an IC-DISC requires deep technical expertise, attention to evolving IRS regulations, and careful strategic planning.

Working with a seasoned specialist, like Paul Ferreira at Export Tax Management, ensures that:

Your IC-DISC is properly structured from the outset.

Commission calculations are maximized within IRS guidelines.

Annual filings, including Form 1120-IC-DISC, are completed accurately and on time.

Ongoing compliance reviews catch small issues before they become costly mistakes.

An experienced IC-DISC advisor also helps you stay ahead of regulatory changes. The IRS occasionally updates procedures and audit priorities, and having a dedicated expert means you remain fully compliant.

Ultimately, the guidance of a specialist can mean the difference between maximizing your export tax benefits—or losing them altogether.

FAQs About IC-DISC Rules

I. What happens if I miss the IC-DISC election deadline?

If you fail to file Form 4876-A within 90 days of incorporating your IC-DISC, you will lose eligibility for that tax year. Under IC-DISC rules, no late elections are permitted. Missing the deadline could cost your company significant export tax savings. To avoid missing critical deadlines, it’s important to work with an experienced IC-DISC advisor. Learn more on our IC-DISC Management page.

II. Can a service company qualify for IC-DISC benefits?

Yes, in some cases. Although IC-DISC benefits primarily apply to the export of tangible goods, certain services—such as architectural and engineering services performed for projects outside the United States—can also qualify. Specific documentation is required to meet IC-DISC qualification standards. See how your business might benefit by reviewing IC-DISC Explained.

III. How often must I review my IC-DISC compliance?

Annual reviews are essential. Even if your IC-DISC was properly formed, IRS guidelines and interpretation of IC-DISC rules can evolve. Regular internal audits, updated documentation, and careful preparation of your IC-DISC Tax Return help protect your benefits and avoid penalties.

Still have questions about setting up or maintaining an IC-DISC?

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Understanding and adhering to IC-DISC rules is essential for any U.S. exporter seeking to unlock substantial federal tax savings. The Interest Charge Domestic International Sales Corporation remains a powerful but highly technical tool, requiring strict compliance across formation, operations, and annual reporting.

Even small mistakes can lead to disqualification or loss of significant tax benefits. That’s why partnering with an experienced IC-DISC specialist is crucial.

Ready to maximize your export tax savings with full IC-DISC compliance?

Contact Us today to schedule a consultation with one of the nation’s leading IC-DISC experts.

Take the first step toward protecting and enhancing your export tax incentives today.

For U.S. exporters, the Interest Charge Domestic International Sales Corporation (IC-DISC) offers a valuable tax benefit—deferred federal income tax on export profits. However, to take full advantage of these savings, companies must adhere to specific regulations, including the IC-DISC Commission Payment Rules, which mandate timely commission payments.

The IC-DISC program is built around the concept of a commission paid by the exporter (related supplier) to the IC-DISC. These commission payments are key to shifting profits to the tax-advantaged IC-DISC, allowing companies to defer taxes on export income. However, to fully benefit from the program, companies must ensure that commission payments are made within strict deadlines. Meeting these deadlines ensures that your business remains compliant with the IC-DISC Commission Payment Rules and can continue to enjoy the valuable tax advantages provided by the program.

There are two key payment deadlines you need to keep in mind:

60 Days After the End of Your Tax Year: A reasonable estimate of the IC-DISC commission must be paid to the IC-DISC by this deadline.

90 Days After Finalizing the Commission: If the initial estimate was insufficient, any remaining unpaid commission must be settled within 90 days of determining the final amount.

In this article, we will walk you through these two critical deadlines under the IC-DISC Commission Payment Rules: the 60-day estimate and the 90-day payment rule, ensuring you stay compliant and maximize your tax benefits.

The 60-Day Rule: Key Payment Deadline for Exporters

Under the IC-DISC Commission Payment Rules, the 60-day rule requires exporters to pay a reasonable estimate of the IC-DISC commission within 60 days after the close of their tax year.

This estimate is a critical step in maintaining compliance with the program and ensures that exporters continue to receive the tax benefits associated with the IC-DISC.

Here’s what you need to know about the 60-day rule:

1. Why the 60-Day Rule Exists

The primary purpose of the 60-day rule is to give the exporter a chance to estimate their commission payment to the IC-DISC, even if the final commission amount has not been calculated yet. By making an initial payment within 60 days, the exporter demonstrates their good faith effort to comply with the rules, while also ensuring that the IC-DISC can benefit from the tax deferral on export profits.

2. Estimating the Commission

At this stage, the exporter may not have access to the full data needed to determine the final commission. However, a reasonable estimate based on available information is required. The estimation process might involve:

Projecting total export sales for the year.

Estimating net income attributable to exports.

Using past data to forecast expected commission amounts.

The goal is to get as close as possible to the final amount, but it’s important to remember that this is an estimate, and it does not need to be precise.

3. Safe Harbor Provision

The IRS provides a “safe harbor” provision for exporters. This allows a minimum payment of 50% of the final commission amount to be considered reasonable. This means that exporters can pay 50% of what they expect the final commission will be without fear of penalties, even if the actual final commission differs.

However, while the 50% minimum is acceptable, it’s highly recommended that exporters pay a higher percentage if possible. Paying more than 50% ensures flexibility when it comes to the finalization of the commission calculation, and it helps to avoid any risk of non-compliance.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Here’s a simple process to follow to comply with the 60-day rule:

Step 1: Review your export sales data for the year to estimate total export revenue. Step 2: Calculate or estimate the net income attributable to export sales (if using the 50% of net income method). Step 3: Apply the appropriate IC-DISC commission calculation method (either 4% of gross receipts or 50% of net income).

Step 4: Pay the estimated commission amount to the IC-DISC within 60 days of the tax year-end.

Step 5: Keep detailed records of the estimation process, including the methodology and data used, to provide transparency and ensure compliance.

5. Benefits of Paying More Than 50%

While the IRS allows the minimum payment of 50%, paying more offers several benefits:

Flexibility in final calculations: The higher the estimate, the less likely the exporter will need to make a significant adjustment later.

Smoother cash flow management: Making a higher payment early can help avoid a large, unexpected payment later.

Minimized risk of penalties: Paying more than the minimum ensures that exporters stay ahead of any potential underpayment penalties.

6. Example of a 60-Day Rule Payment

Let’s say your company expects that the final IC-DISC commission will be $100,000. Under the 60-day rule, you can pay a minimum of $50,000 (50% of the expected commission) to the IC-DISC within 60 days of the tax year-end. However, if your company can afford to do so, it’s a best practice to pay more—perhaps $70,000 or $80,000—to ensure flexibility and avoid complications later.

7. Possible Consequences of Non-Compliance

If a company fails to meet the 60-day deadline or does not make a reasonable estimate, the IRS may impose penalties or deny the benefits of the IC-DISC program. This could lead to:

Loss of the tax deferral benefit for export profits.

Potential penalties or interest charges for late payments.

A more complicated audit process, which could trigger a more detailed examination of the company’s financial records.

External Source for Further Information

For more detailed information about compliance and the IRS’s requirements regarding the 60-day rule and other aspects of the IC-DISC program, you can refer to the IRS IC-DISC Audit Guide.

Visual Breakdown of the 60-Day Rule Process:

Step

Action

Deadline

1. Estimate Commission

Calculate or estimate the IC-DISC commission.

Within 60 days of tax year-end

2. Make Payment

Pay a reasonable estimate of the commission.

Within 60 days of tax year-end

3. Keep Records

Document the estimation methodology and data used.

Ongoing, for audit purposes

4. Finalize Payment

Adjust if necessary after final commission determination.

Within 90 days (after final determination)

The 90-Day Rule: Finalizing Your IC-DISC Commission Payment

The 90-day rule comes into play after the initial estimate has been made under the IC-DISC Commission Payment Rules. It ensures that the exporter pays the full commission amount to the IC-DISC within 90 days after the final commission calculation is determined.

Here’s a breakdown of what the 90-day rule entails:

1. When the 90-Day Rule Applies

The 90-day rule kicks in after the final commission amount has been calculated. This calculation is typically made when the exporter files their IC-DISC tax return (Form 1120-IC-DISC). The final commission may differ from the initial estimate, either higher or lower, depending on the actual export sales and profit margins.

Once the final amount is determined, the exporter has 90 days to pay any remaining balance to the IC-DISC. This is to ensure that the full commission, as calculated at the end of the tax year, is paid within a reasonable timeframe.

2. Finalizing the Commission Payment

Here’s how the process works for finalizing the commission payment:

Step 1: Once your tax return is filed and the final IC-DISC commission is determined, review the difference between the initial estimate and the final amount.

Step 2: If there is an underpayment (i.e., the initial estimate was too low), make the remaining payment to the IC-DISC within 90 days of the final determination.

Step 3: Ensure the final payment is made before the deadline to avoid potential penalties or issues with the IRS.

3. Ensuring Compliance with the 90-Day Rule

To remain compliant with the 90-day rule, follow these steps:

Monitor the commission determination process: After submitting your IC-DISC tax return, keep an eye on any changes in the final commission.

Make timely payments: Be proactive in making any additional payments needed to cover the difference between the estimated and final commission.

Keep detailed records: Document any adjustments made between the estimated and final amounts to provide a clear audit trail.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

4. Potential Consequences of Not Complying with the 90-Day Rule

Failure to comply with the 90-day rule can result in:

Loss of tax benefits: Not paying the final commission amount within the required timeframe could lead to the forfeiture of the tax deferral benefits offered by the IC-DISC program.

IRS penalties: The IRS may impose penalties or interest for late payments.

Complicated audit process: Non-compliance could trigger a more in-depth audit, increasing the risk of errors or discrepancies in your IC-DISC filings.

5. Benefits of Paying the Final Commission Early

While the 90-day rule gives exporters 90 days to make the final payment, there are several reasons to consider paying the balance sooner:

Avoiding penalties: Paying early helps to ensure compliance and avoid any penalties or interest from the IRS.

Easier financial planning: Making the payment sooner rather than later simplifies your company’s cash flow and financial planning.

Clear recordkeeping: Settling the full commission promptly makes it easier to close out the tax year and track IC-DISC-related payments.

6. Example of the 90-Day Rule in Action

Imagine your initial estimate for the IC-DISC commission was $50,000. After filing your IC-DISC tax return, you determine that the final commission amount is actually $60,000. According to the 90-day rule, you must pay the remaining $10,000 within 90 days of the final determination.

If you fail to make the additional payment within the required 90-day window, you risk losing the tax deferral on export profits and may be subject to penalties.

External Source for Further Information

For more detailed guidance on IC-DISC compliance and payment rules, you can refer to the IRS IC-DISC Audit Guide, which provides additional details about the process and how to remain compliant.

Visual Breakdown of the 90-Day Rule Process:

Step

Action

Deadline

1. Final Commission Determination

Review the final IC-DISC commission once the tax return is filed.

After tax return filing

2. Payment of Remaining Balance

Pay any additional balance between the estimate and final commission.

Within 90 days of determination

3. Keep Detailed Records

Document the final payment and adjustments.

Ongoing, for audit purposes

IC-DISC Commission Calculation Methods: Choosing the Best Approach

Under the IC-DISC Commission Payment Rules, exporters have two primary methods for calculating their IC-DISC commission:

4% of Gross Receipts Method

50% of Net Income from Exports Method

Method

Commission Calculation

Example

4% of Gross Receipts

4% of total export sales revenue

$5M export sales = $200,000 commission

50% of Net Income from Exports

50% of net income from export sales after costs and expenses

$1M net income = $500,000 commission

Let’s break down both methods:

4% of Gross Receipts Method

This method sets the commission at 4% of total export sales revenue.

Advantages:

Simple: Easy to calculate based on total export sales.

Predictable: Provides a straightforward estimate for compliance with the 60-day rule.

Example: If your export sales were $5 million, the commission would be $200,000 ($5,000,000 * 4%).

50% of Net Income from Exports Method

This method calculates the commission as 50% of the net income from export sales, after accounting for costs like COGS.

Advantages:

Tax efficiency: Suitable for businesses with high export costs.

Profit-based: Reflects actual profitability.

Example: If net income from exports was $1 million, the commission would be $500,000 ($1,000,000 * 50%).

Choosing the Best Method for Your Business

Profit margins: The 50% of Net Income Method is best for companies with lower profit margins.

Simplicity: The 4% of Gross Receipts Method is simpler and easier to apply.

Consistency: Once you choose a method, try to stick with it for consistency.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Simple vs. Transaction-by-Transaction (TxT) Calculations

While the 4% of Gross Receipts and 50% of Net Income from Exports methods offer straightforward approaches for calculating IC-DISC commissions, some exporters may prefer a more precise method that reflects the profitability of individual export transactions. This is where the Transaction-by-Transaction (TxT) method comes into play.

What is the TxT Method?

The TxT method allows exporters to calculate their IC-DISC commission on a per-transaction basis. This method takes into account specific factors like:

The cost of goods sold (COGS) for each export transaction.

Margins specific to each export sale.

Any unique transaction-related expenses or adjustments.

By using the TxT method, exporters can achieve a more accurate reflection of the profitability of each export transaction, rather than relying on broader estimates based on overall sales.

When Should You Use the TxT Method?

The TxT method is ideal for businesses that:

Have a wide range of different export transactions with varying profit margins.

Want to maximize the accuracy of their IC-DISC commission and potentially reduce tax liabilities by focusing on individual transaction profits.

However, it requires more detailed tracking and a robust accounting system to calculate commission on a transaction-by-transaction basis.

Compliance Considerations for TxT Method

If you choose to use the TxT method, it’s important to ensure compliance with all applicable regulations. Any errors or omissions in transaction calculations could lead to non-compliance and disqualification from IC-DISC benefits. For more information on the potential consequences of non-compliance, check out our guide on IC-DISC Disqualification from Benefits.

Additionally, be aware that if you’re paying IC-DISC dividends, they must meet certain requirements to qualify as tax-advantaged. For more on IC-DISC dividends, refer to our article on Are IC-DISC Dividends Qualified?.

Compliance and Penalties

Failure to comply with the IC-DISC Commission Payment Rules can lead to significant consequences, including the loss of tax deferral benefits and penalties from the IRS. To avoid these risks, it’s crucial to stay on top of your commission payments and deadlines.

Consequences of Missing the 60-Day or 90-Day Deadlines

If you fail to meet either the 60-day or 90-day payment deadlines, your company may face the following penalties:

Loss of IC-DISC Benefits: If you miss the required deadlines, you could lose the tax advantages that come with the IC-DISC program. This means you will no longer be able to defer federal income tax on export profits.

IRS Penalties: The IRS may impose penalties for failing to make timely payments. These penalties can add up quickly and result in substantial financial consequences.

The best way to avoid these penalties is by establishing a clear process for calculating and making commission payments. Regular monitoring of your export sales and commission calculations throughout the year will help ensure that you meet the necessary deadlines.

The Importance of Accurate Recordkeeping

Accurate recordkeeping is vital for ensuring compliance. Keeping detailed documentation of your export sales and commission calculations helps demonstrate that you made a good faith effort to comply with the IC-DISC Commission Payment Rules. Proper records can also be invaluable if your company faces an IRS audit.

This documentation should include:

The methodology used for commission calculations (e.g., 4% of Gross Receipts or 50% of Net Income from Exports).

Supporting data for your estimated commission payments.

Any adjustments made after final commission determination.

How to Protect Your IC-DISC Benefits

To ensure that you retain the full tax benefits of the IC-DISC program, here are a few best practices:

Review Your Export Sales Regularly: Regularly reviewing your export sales data allows you to stay ahead of any potential underestimations or overestimations of the commission, making it easier to pay within the required deadlines.

Set up Alerts for Deadlines: Use reminders and alerts to help you keep track of critical IC-DISC payment deadlines (60 days and 90 days).

Consult With Tax Advisors: Working with tax professionals who specialize in IC-DISC regulations ensures that you remain compliant and that you make the most of the program’s tax savings. To learn more about the potential penalties for missing IC-DISC payment deadlines, visit our guide on IC-DISC Commission Payment Due Date and Disqualification.

Best Practices for Managing IC-DISC Commission Payments

To ensure compliance with the IC-DISC Commission Payment Rules and maximize tax benefits, follow these best practices:

Regular Reviews of Export Sales Data

Quarterly Reviews: For steady export activity, review your sales data quarterly.

Frequent Reviews: For businesses with high transaction volume, consider monthly or bi-monthly reviews to ensure accurate commission estimates.

Standardized Process for Commission Calculations

Consistent Method: Use a clear and consistent calculation method, whether it’s the 4% of Gross Receipts Method or 50% of Net Income from Exports Method.

Track Adjustments: Document any changes to your initial estimate, especially if using the Transaction-by-Transaction (TxT) Method.

Clear Communication Across Your Team

Set Deadlines: Ensure everyone is aware of key deadlines and commission amounts.

Consult Tax Advisors: Work with tax professionals to stay compliant and fully leverage IC-DISC benefits.

Financial Planning for IC-DISC Commission Payments

Reserve Account: Set up a dedicated reserve account to ensure funds are available when needed. Incorporate into Budgeting: Include IC-DISC commission payments in your financial planning to avoid last-minute stress.

Seek Expert Guidance

For expert advice and assistance with managing your IC-DISC payments, contact us. We’re here to help you optimize your IC-DISC benefits and stay compliant.

Financial Planning for IC-DISC Commission Payments

Effective financial planning ensures timely and accurate IC-DISC commission payments, helping you stay compliant with the IC-DISC Commission Payment Rules.

Start by setting aside funds early. Consider establishing a dedicated reserve account for IC-DISC commissions, which guarantees that you have the necessary funds available and helps avoid financial strain as payment deadlines approach.

Incorporate IC-DISC payments into your annual budget to forecast expenses and ensure smooth cash flow. This proactive approach reduces surprises and ensures you’re prepared.

It’s also a good idea to work with a tax advisor experienced in IC-DISC regulations. They can help optimize tax savings, keep you compliant, and ensure that your financial planning aligns with IC-DISC requirements.

For personalized guidance, feel free to contact us.

FAQs

I. What is the difference between the 60-day and 90-day IC-DISC commission payment rules?

The 60-day rule requires a good faith estimate of the IC-DISC commission to be paid within 60 days of the tax year-end. The 90-day rule addresses any remaining balance after the final commission amount is determined. You essentially have 90 days to settle any outstanding commission owed to the IC-DISC after finalizing the commission amount.

II. Are there any exceptions to the IC-DISC commission payment deadlines?

Currently, there are no formal exceptions to the IC-DISC commission payment deadlines. However, if extenuating circumstances prevent meeting the deadlines, it’s recommended to consult with a tax advisor. They can help navigate potential options or assist in working with the IRS if necessary.

III. How often should I review my export sales data to ensure accurate IC-DISC commission calculations?

Regularly reviewing your export sales data is crucial for accurate commission calculations. The frequency of reviews depends on your business volume and transaction complexity:

Quarterly reviews may be sufficient for companies with steady export activity. Monthly or bi-monthly reviews are beneficial for businesses with high transaction volumes or significant fluctuations in export sales.

IV. What are the benefits of setting up a dedicated reserve account for IC-DISC commission payments?

A dedicated reserve account offers several advantages:

Ensured funds availability: It guarantees you have the necessary resources to meet deadlines without disrupting cash flow. Financial planning: Helps in budgeting and forecasting commission expenses. Discipline and compliance: Fosters consistent adherence to IC-DISC commission requirements.

Have more questions about IC-DISC commission payments?

Export Tax Management offers expert guidance on IC-DISC regulations and commission calculations. Contact us today to discuss your specific situation and ensure you’re maximizing the tax benefits of the IC-DISC program.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Understanding and adhering to the IC-DISC Commission Payment Rules is crucial for U.S. exporters who want to maximize their tax benefits. By making timely commission payments and staying compliant with the 60-day and 90-day deadlines, you can defer taxes on export profits and enjoy significant savings.

To ensure compliance, it’s essential to establish clear processes, review export sales regularly, and maintain accurate records. You should also work closely with tax advisors who specialize in IC-DISC to optimize your tax benefits.

If you have questions or need assistance with IC-DISC commission payments, don’t hesitate to contact us. We’re here to help you navigate the process and ensure you’re taking full advantage of the IC-DISC program.

One key requirement is IRS Form 8404, Interest Charge on DISC-Related Deferred Tax Liability, which calculates the interest charge on deferred taxes tied to IC-DISC profits.

Helps businesses avoid IRS penalties and maintain compliance.

Supports proper tax planning for exporters benefiting from IC-DISC structures.

With IC-DISC tax savings reaching up to 20% for qualifying exporters ([source]), understanding Form 8404 is crucial.

This guide will explain its purpose, filing requirements, and best practices to ensure compliance.

Who Needs to File Form 8404?

IRS Form 8404 is specifically required for IC-DISC shareholders.

An IC-DISC, or Interest Charge Domestic International Sales Corporation, is a tax incentive structure that allows U.S. companies to defer paying taxes on profits derived from export sales. These deferred taxes accumulate, and Form 8404 calculates the interest on those deferred amounts.

If you’re a shareholder in an IC-DISC, whether you’re a corporation, partnership, or individual, it’s crucial to file this form. Failing to do so can lead to unnoticed interest accrual, resulting in substantial penalties.

In essence, it helps maintain transparency and accountability for IC-DISC shareholders, ensuring they fulfill their tax obligations on time (Learn more about IC-DISC requirements from the IRS.)

Need help with your IC-DISC filings? Our expert team can simplify the process. Contact us today for a free consultation and keep reading to find out more useful information:

What is the Purpose of Form 8404?

Form 8404 is essential for the IC-DISC structure, as it calculates the interest charge on deferred taxes. This form ensures that businesses comply with IRS regulations while benefiting from tax deferrals.

1. Tax Liability Management

IC-DISC allows businesses to defer federal taxes on export income, reducing immediate tax burdens. However, interest accrues on the deferred taxes, and Form 8404 calculates the amount owed.

Example: If a company defers $1 million in taxes, Form 8404 determines the interest on that deferred amount.

2. IRS Compliance

Form 8404 ensures businesses pay the correct interest on deferred taxes, keeping them compliant with IRS regulations and avoiding penalties.

Example: A company that forgets to update Form 8404 could face penalties for underreporting interest owed.

3. Tax Benefits Example

By deferring taxes, businesses can reinvest savings into growth or distribute funds to shareholders at lower tax rates.

Example: A manufacturer exports $5 million worth of products, defers $500,000 in taxes, and uses the savings for expansion.

Maximizing your tax savings while staying compliant is crucial. Learn more about our IC-DISC Incorporation and Implementation services to ensure your business benefits from IC-DISC tax incentives.

Filing Instructions for Form 8404

Filing IRS Form 8404 can be daunting if you’re unfamiliar with the process. Below is a step-by-step guide to help you through it:

Gather Required Information: You’ll need financial records of the deferred IC-DISC income and any previous interest charges paid.

Complete Section I – Interest Charge: This section calculates the interest due on your deferred IC-DISC taxes. Be sure to input the correct deferred tax amount and use the applicable interest rates set by the IRS for the specific tax year.

Complete Section II – Adjustments: If there are any overpayments or adjustments from previous filings, they should be reported here.

Final Review and Submission: Double-check all figures before submitting. Accuracy is essential to avoid triggering an IRS audit or penalty.

For those unfamiliar with the nuances of Form 8404, consider contacting our team at Export Tax Management. We offer comprehensive filing services to ensure your company maximizes its IC-DISC tax benefits while staying fully compliant.

If you’re also preparing your IC-DISC’s annual return, be sure to check out our guide on Form 1120-IC-DISC and Schedule P, crucial components for IC-DISC compliance.

20+ Years IC-DISC Experience

Unlock Significant Tax Benefits with IC-DISC

Our objectives are simple: to provide you with maximum export tax savings, while delivering unmatched personal attention by our staff of CPAs. Schedule a free consultation today to discuss how Export Tax Management can help you.

Step-by-Step Filing Example: How to Complete Form 8404

Filling out IRS Form 8404, Interest Charge on DISC-Related Deferred Tax Liability, is essential for IC-DISC shareholders to report and pay the required interest charge on deferred tax liabilities.

Below is a step-by-step guide using a hypothetical example to clarify the process.

Example Scenario

ABC Exports is an IC-DISC shareholder that has deferred $500,000 in taxable income from export sales. The IRS-designated interest rate for deferred tax liabilities this year is 4%. To comply with IRS regulations, ABC Exports must calculate the interest charge and submit the Form along with the payment.

Step 1: Enter Taxpayer Information

At the top of Form 8404, the taxpayer must provide basic details, including:

Taxpayer Name: ABC Exports

Address: 123 Business Ave, New York, NY 10001

Taxpayer Identification Number (TIN): 12-3456789

Tax Year: 2023

This section ensures the IRS correctly associates the filing with the appropriate shareholder.

Step 2: Calculate the Interest Charge

The primary purpose of Form 8404 is to determine the interest owed on deferred IC-DISC income. This requires:

Line 1: Enter the total deferred DISC income → $500,000

Line 2: Enter the IRS-designated interest rate → 4%

Line 3: Multiply Line 1 by Line 2 to calculate the interest charge:

$500,000 × 4% = $20,000

This means ABC Exports owes a $20,000 interest payment for the deferred tax liability.

Step 3: Provide Payment Details

Once the interest charge is calculated:

Confirm the total amount due (in this case, $20,000).

Prepare the payment according to IRS instructions (check, electronic payment, or other accepted methods).

Ensure all details are correct before submitting the form.

Step 4: Sign and Submit the Form

Before submission:

Double-check all entries for accuracy.

The responsible shareholder must sign and date the form to certify correctness.

Submit Form 8404 by the required IRS deadline to avoid penalties.

By following these steps, IC-DISC shareholders can ensure accurate filing and compliance with IRS regulations. Proper completion of Form 8404 helps avoid penalties and keeps businesses in good standing with tax authorities.

Deadlines and Penalties

The filing deadline for Form 8404 is aligned with the filing of the IC-DISC tax returns. Typically, the form should be filed by April 15th for shareholders, but if the IC-DISC operates under a fiscal year rather than a calendar year, this deadline may vary.

Missed Deadlines and Penalties:

Late Filing Penalty: Failing to file Form 8404 on time can result in penalties, which are calculated based on the interest that should have been paid.

Accrued Interest: Delayed filings may cause additional interest to accumulate on deferred taxes, increasing the company’s tax liability.

To avoid these pitfalls, ensure you have a system in place for timely submission.

Filing IRS Form 8404 correctly is crucial to avoid IRS audits and penalties. Certain mistakes or inconsistencies can raise red flags that might lead to a tax audit. Here are the most common audit triggers associated with Form 8404:

1. Consistently Miscalculating Deferred Interest

One of the most common issues that can trigger an IRS audit is consistently miscalculating the interest charge on deferred IC-DISC income. If the interest rate or the amount of deferred income is incorrectly reported, the IRS may flag your return for further scrutiny.

Tip: Double-check your interest calculations and ensure the correct IRS interest rate is applied for the tax year. (IRS Interest Rates)

2. Failing to Update Prior Year Adjustments

If adjustments from prior years are not reflected in the current filing, this can lead to discrepancies and raise concerns with the IRS. It is critical to update it with any deferred amounts or adjustments from previous filings.

Tip: Regularly review your prior year filings and ensure all adjustments are carried over accurately. (IRS Form 8404 Instructions)

3. Reporting Inconsistencies Between Form 8404 and Other IC-DISC Filings

Reporting inconsistencies between Form 8404 and other IC-DISC-related forms (such as Form 1120-IC-DISC) can trigger an audit. The IRS cross-references data from multiple forms, and discrepancies can signal errors or intentional misreporting.

Tip: Ensure consistency across all forms, and use reliable accounting practices to prevent misreporting.

4. Failure to Include Required Supporting Documentation